The goal of “No Surprises.”

Hurricane Helene has now been downgraded to a tropical storm with sustained winds of 45 mph centered about 30 miles southwest of Bryson City, NC. Movement is heading towards the North at 32 mph. This is after a devastating night along the Gulf Coast when Hurricane Helene came ashore at 11:10 pm EDT near the mouth of the Aucilla River as a Category 4 hurricane with a pressure of 938 mb and sustained winds of 140 mph. According to the preliminary data, this means Helene had a lower pressure than Hurricane Ian (2022) at landfall, which was 941 mb. However, the forward speed of Helene at landfall was 24 mph, which was faster than Charley's (2004) 21 mph.

The goal of these tropical updates is to support the insurance industry with “No Surprises.” These posts are not meant to replace the great content that the National Weather Service and National Hurricane Center produce. There is no need to cut and paste the content the insurance industry should already be following. These posts aim to offer fresh insights beyond typical discussions, with a focus on connecting impacts to the insurance industry. Each event is unique and complex, and Helene is no exception. It is impossible to capture every detail of the event. Still, our aim is to highlight key aspects that might not be covered by other media, such as the treefall, low housing and building density in the landfall areas, saturated ground, the sensitivity of storm tracks on insurance losses, building codes, and the potential response of catastrophe risk models, among others.

It was well known that Helene could grow into a monster of a storm. Various forecast models, which are continually improving, were on target several days in advance in this case. There is still some work to do on intensity. Still, again, the scenarios of a major hurricane, including Category 4, were on the table days in advance, even before Helene was named. The sea surface temperature are not 100% at fault for this increase in intensity, which was at or near record levels. Many other factors have to be perfect. In the case with Helene the upper-level dynamic “venting,” low wind shear, and plenty of moisture at various levels of the atmosphere provide the perfect ingredients for the strengthening that the other storms did not have this year upon landfall.

In the last 13 months, Taylor County, FL, has experienced all of Florida's landfalls: Helene, Idalia, and Debby, a truly remarkable occurrence. Helene’s landfall in the Big Bend of Florida is the strongest hurricane to make landfall in the area on record (since 1851). The old record was held by the Cedar Keys Hurricane (1896), with max winds of 125 mph. Helene’s Category 4 landfall gives the U.S. a record eight Category 4 or Category 5 Atlantic hurricane landfalls in the past eight years (2017-2024), seven of them being continental U.S. landfalls. Underscoring the severity of this event is a remarkable turnaround after the 10-year major hurricane drought between 2006 and 2016.

Catastrophe Is Still Unfolding

Today, the catastrophe is still unfolding, particularly in the Appalachian Mountains. As Helene tracks up into the lower Ohio River valley, strong upslope winds will occur over the Appalachians. However, the most significant story is the record rainfall and widespread flooding expected across the region, particularly in areas like Asheville, NC. Even more unexpected are the predicted landslides. Overall, this region is likely to experience its worst disaster in modern times, with flooding potentially surpassing the historic floods of 1916. For more local info on river levels and rainfall use https://water.noaa.gov/

One cannot downplay the wind impacts that have already occurred with Helene and will occur today as it continues to weaken into areas that do not experience many tropical-storm-force winds. Over 3 million customers are already without power as strong winds and tree falls have taken their toll on the power grid. In fact, Helene once again points out that water is the new wind. Combined with the inland flooding and the record storm surge that was verified along the a large section of the western Gulf Coast, this will be a very costly economic event. The preliminary data shows storm surge records were crushed from Cedar Key to Sarasota, which is disastrous and beyond words. Still, this was anticipated due to Helene’s large size and the region’s bathymetry, with the Gulf of Mexico’s gradual, shallow incline towards the coast amplifying water levels with onshore winds. Many were likely surprised by the storm surge's height as far south as Fort Myers Beach, which recorded its second-highest water level at 5.12 feet in Southwest Florida in over 60 years—just below Hurricane Ian's 7.5 feet in 2022. This observation can be found in the NOAA Hurricane Helene Coastal Inundation dashboard.

Unfortunately, according to the NFIP data, most inland counties in Georgia and the Carolinas have flood insurance take-up rates of less than 1%, and the Big Bend region that experienced the high storm surge is less than 10%. Even in parts of the Tampa Bay area, the take-up rates are only 25%. This means that in general, Helene will once again show there is a growing production gap as a lot of flooded properties will be uninsured losses.

Aside from the strongest winds in Georgia's Big Bend region, much of the wind damage may fall below the higher named storm deductibles, as most structures are built to withstand tropical-storm-force winds. The strongest winds seemed to avoid the Atlanta area, which only had wind gusts of 43 mph. However, Augusta, GA, which is to the east, had a gust of 82 mph. As pointed out, the key to insurance losses might have been how close the strongest winds got to Tallahassee, and it would appear Tallahassee only had a wind gust of 67 mph, and Gainesville had a wind gust of 63 mph. The Perry Airport, located in Florida, experienced a wind gust of 99 mph. As shown in the BMS iVision below, the strongest winds impacted one of the region's lowest housing/population densities, if not the entire U.S. coastline.

Windy.com is a great tool for quickly reviewing wind observations. Simply click on a weather station and look for the maximum wind gust, which should show up in the timeline if that weather variable is logged.

Hurricane & Learnings for the Insurance Industry

The catastrophic model event sets from the last few days likely had event selected that were two far-west with Helene's track. However, the insurance industry also needs to remember that these models likely do not have events that match Helene's forward speed, size, and intensity, and it will be a few days before they can provide realistic events for loss estimates that match Helene's unique characters. There will no doubt be modeling challenges, such as the strong inland wind over Athens, GA and August, GA, that seem to have resulted in an enormous amount of tree fall, adding to the complexity of estimating the insured loss, which is typically not handled well in catastrophic risk models.

The insurance industry learns from every event. Similar to what we witnessed with Francine and its impacts on the populated New Orleans Area and how it recovered from Ida, Helene will provide a great case study of how resilience increased in the rebuilding efforts from Hurricane Idalia in just 13 months. Another important aspect is the new data and insights the insurance industry will gain from storms like Helene. For instance, the Texas Tech University research team deployed StickNets ahead of the storm to collect various measurements in areas where weather data is typically scarce. The Doppler on Wheels travelled down from the central plains and stationed itself at the Perry Airport to fill in any radar gaps and other low-level measurement to better understand the storm structure. In addition to the constant flights from the multiple hurricane hunters, the NOAA hurricane hunters are now flying uncrewed hurricane-hunting drones. From inside the eye of Category 4 Helene last night, scientists measured 10-second flight-level winds of 158 mph at 946 mb as the drone skimmed the ocean. Of course, this is preliminary data, but either way, it is remarkable how we capture more information. All this scientific data can then be used against lost data to better understand future events for the insurance industry.

As previously mentioned, we will examine how recent events and damages have improved or mitigated insurance losses where "build-back-better" approaches were implemented. Quick storm mitigation with better-advanced forecasting can also limit the damage. Perhaps one of the best examples of this was the AquaFense that was put up at Tampa General Hospital, which is a water-impermeable barrier designed to withstand storm surges up to 15 feet. This prevents heavy rain events and surge storm events from impacting hospital operations.

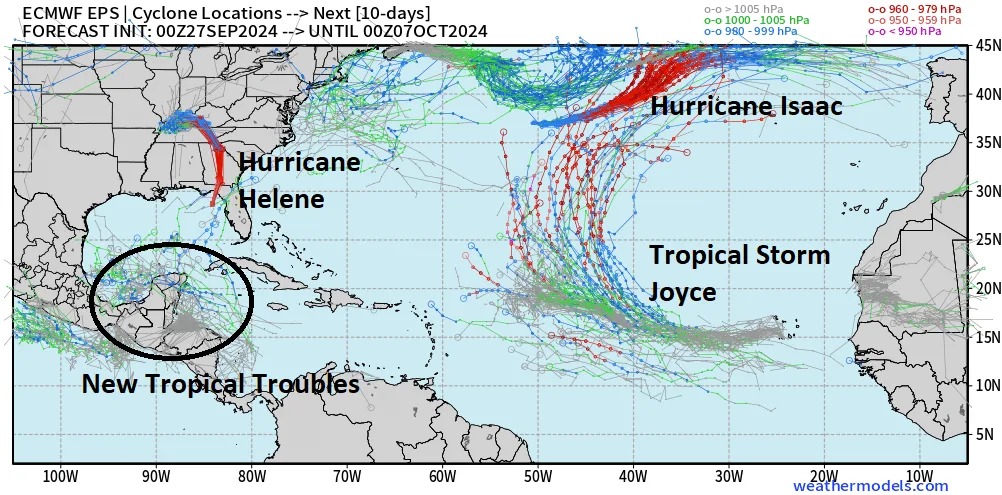

Exhale And Hold Your Breath Later Next WeekThe season is not over yet, and the insurance industry has about a week to catch its breath. By late next week, attention will turn back to the same area in the Gulf of Mexico where Helene developed. With the MJO in favorable phases, early October could see heightened activity before the basin calms down and conditions return to normal.